Lead Story · Books

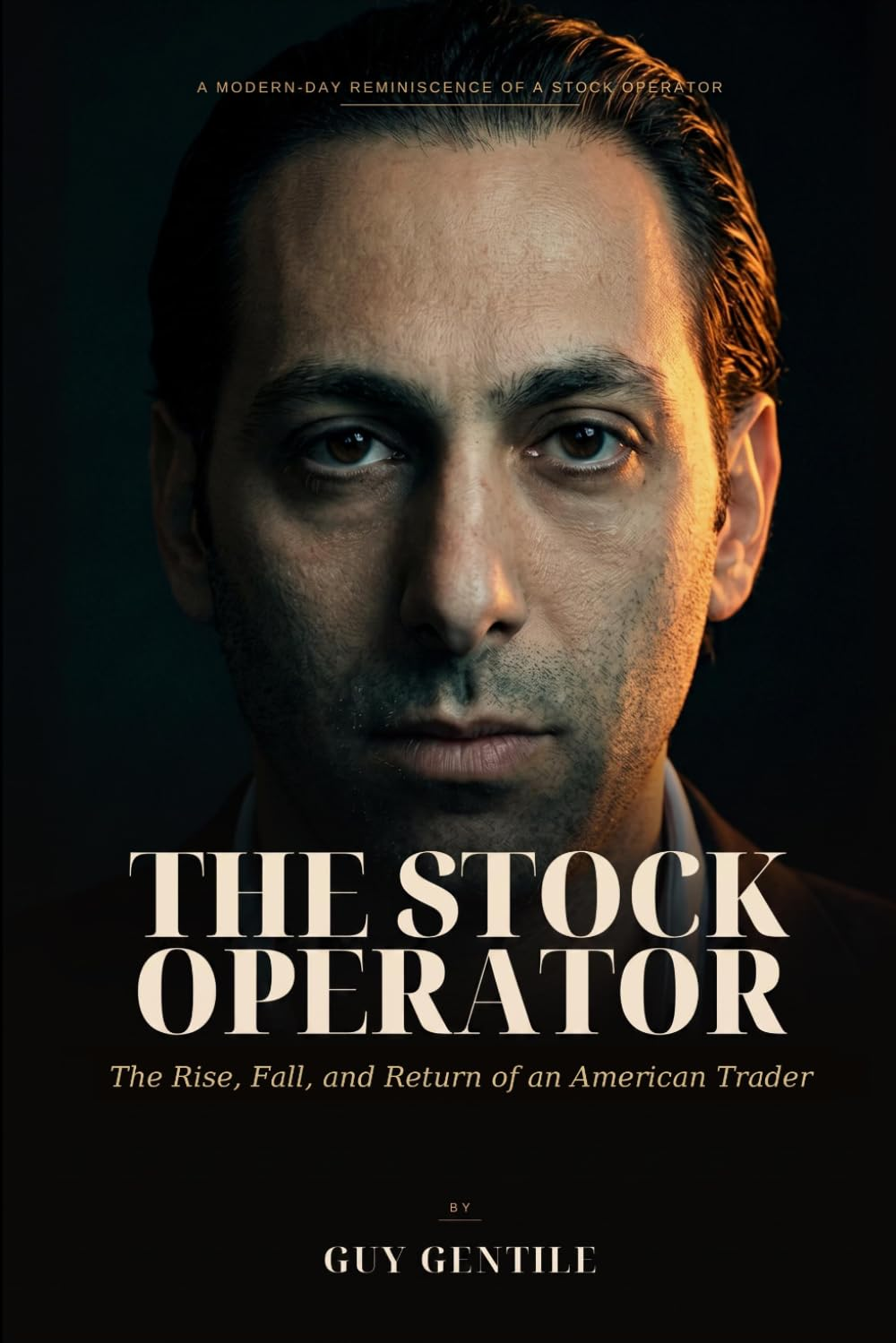

The Stock Operator — Guy Gentile's New Book on How He Actually Trades

Twenty-five years on the desk, compressed into one book: the momentum and short-selling playbook, the risk rules, and the daily routine behind the trades. Out now — read the inside story and get your copy.